Ultimate Guide On How The Economy Works

Table of Interests

Looking for the best article on The Economy?, then “Ultimate Guide On How The Economy Works”, is for you.

- Credit – money you receive that you must repay later – powers the economy.

- More credit means more spending. More spending means more income, and more income means more credit is available from lenders.

- Credit also creates debt: the borrowed money must be paid back, so spending must decrease later.

- Governments raise and lower interest rates to keep the economy in check.

Introduction

The economy makes the world go round. It deeply affects each of us in our daily lives, so it’s certainly something worth understanding, even at a high level.

Definitions of “the economy” vary, but, broadly speaking, an economy could be described as an area where goods are produced, consumed, and traded. Typically, you’ll see them discussed at the national level, with op-eds and news reporters referencing the U.S. economy, the Chinese economy, etc. However, we can also look at economic activity through a global lens by taking into account every country’s activities and affairs.

In this piece, we’ll dive into the concepts that make up an economy, drawing on Ray Dalio’s model (explained in How the Economic Machine Works).

Who makes up the economy?

Let’s begin at a small scale before working our way up. Every day, we contribute to the economy by buying (i.e., groceries) and selling (i.e., working in exchange for payment). Other individuals, groups, governments, and businesses worldwide do the same across three market sectors.

The primary sector concerns itself with the extraction of natural resources. Here, you have things like chopping down trees, mining gold, and farming (to name just a few examples). This material is then used in the secondary sector, which is responsible for manufacturing and producing. Lastly, the tertiary sector covers services from advertising to distribution.

The “three-sector” breakdown is the generally agreed-upon model. However, some have extended it to include a quaternary sector and a quinary sector to further distinguish between services in the tertiary sector.

Measuring economic activity

To determine the health of the economy, we want to be able to measure it somehow. By far, the most popular method for doing so is by using GDP, or Gross Domestic Product. This metric seeks to calculate the total value of goods and services produced in a country in a given period.

Broadly speaking, a rising GDP signifies an increase in production, income, and spending. Conversely, a falling GDP indicates decreasing production, income, and spending. Note that there are a couple of variations you can use: real GDP accounts for inflation, whereas nominal GDP does not.

GDP is still only an approximation, but it carries tremendous weight in analyses at national and international levels. It’s used by everyone from small financial market participants to the International Monetary Fund to gain insight into countries’ economic health.

GDP is a reliable indicator of a country’s economy, but, as in technical analysis, it’s best to cross-reference it with other data to gain a more comprehensive understanding.

Credit, debt, and interest rates

Lenders and borrowers

We touched on the fact that everything boils down to buying and selling. It’s worth noting that lending and borrowing are essential as well. Suppose that you’re sitting on a large amount of cash that isn’t currently doing anything. You might wish to put that money to work so that it can generate more money.

One way of doing this is by lending it out to someone who needs to buy something, such as machinery for their business. They don’t have the cash available currently, but once they buy the machinery, they can pay it back from sales of their finished product. You act as a lender, and the other party acts as a borrower.

To make it worthwhile, you set a fee for lending out your cash. If you lent $100,000, you might say something like “you can have this money on the condition that you pay me 1% for every month that it isn’t repaid.” This additional charge is called interest.

Going with simple interest would mean that the other party owes you $1,000 every month until the money is returned. If it were repaid after three months, you’d expect to receive $103,000, plus whatever additional fee you specified.

By offering that money, you create credit: an agreement that the borrower will repay you later. Credit card users will be familiar with this concept. When making a payment by card, the money isn’t instantly removed from your bank account. It doesn’t even need to be in there, provided you settle your bill afterward.

With credit comes debt. By acting as a lender, you’re owed money, and, by acting as a borrower, you owe money. The debt disappears once the loan is repaid with interest.

Banks and interest rates

Banks are probably the most notable types of lenders in today’s world. You could think of them as middlemen (or brokers) between lenders and borrowers. These financial institutions actually take on the role of both.

When you put money into the bank, you do so on the condition that they’ll give it back to you. Many others do the same. And, since the bank has such a large amount of cash on hand now, it lends it out to borrowers.

Of course, that means that the bank won’t hold all of the money it owes at once. It operates a fractional reserve system. It could be problematic if everyone asked for their money to be returned at the same time, but that rarely happens. When it does, though (e.g., if everyone loses faith in the bank), a bank run occurs, potentially causing the bank to collapse. The U.S. Great Depression bank runs of 1929 and 1933 are good examples.

Banks typically offer you an incentive to lend them your money in the form of interest rates. Naturally, higher interest rates will be more attractive to lenders (as they’ll get more money). To borrowers, the opposite applies – lower interest rates mean that they won’t need to pay as much on top of the principal sum.

Why is credit important?

Credit could be seen as a kind of lubricant for the economy. It allows individuals, businesses, and governments to spend with money that they don’t have immediately available. To some economists, this is problematic, but many believe that increased spending is a sign of a thriving economy.

If more money is being spent, more people receive an income. Banks are more inclined to lend to those with higher incomes, meaning that individuals now have access to more cash and credit. With more cash and credit, individuals can spend more, meaning that more people receive an income, and the cycle continues.

Of course, this cycle can’t just continue indefinitely. By borrowing $100,000 today, you deprive yourself of $100,000+ tomorrow. So, while you can temporarily increase your spending, you’ll eventually have to decrease your spending to pay it back.

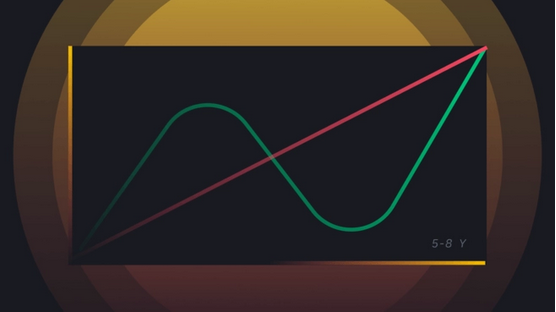

Ray Dalio describes this concept as the short-term debt cycle, illustrated below. He estimates that these patterns repeat themselves over 5-8 year periods.

In red is productivity, which grows over time. In green is the relative amount of credit available.

So what are we looking at, exactly? Well, let’s first note that productivity is steadily increasing. Without credit, we’d expect that to be the only source of growth – after all, you would need to produce to receive income.

In the first part of the chart, we can see that because of credit, income grows faster than productivity (causing economic expansion). Eventually, the expansion halts and leads into economic contraction. In the second part, the availability of credit significantly decreases as a consequence of the initial “boom.” As a result, obtaining loans is more difficult, and inflation sets in, prompting the government to take remedial measures.

Let’s explore this more in the next section.

Central banks, inflation, and deflation

Inflation

Suppose that everyone has access to lots of credit (part one of the previous section’s graph). They can buy a lot more than they would be able to without it. But while spending is growing skyrocketing, production isn’t. In effect, the supply of goods and services does not materially increase, but its demand does.

What happens next is inflation: this is when you start to see the prices of goods and services increase due to higher demand. A popular indicator for measuring this is a Consumer Price Index (CPI), which tracks the prices of typical consumer goods and services over time.

How does a central bank work?

The banks we described earlier are generally commercial banks – they cater mainly to individuals and businesses. Central banks are government entities responsible for managing a nation’s monetary policy. In this category, you have financial institutions like the United States’ Federal Reserve, the Bank of England, the Bank of Japan, and the People’s Bank of China. Notable functions include adding to the money in circulation (via quantitative easing) and controlling interest rates.

Increasing interest rates is something that central banks might do when inflation gets out of hand. When rates are increased, the interest owed is higher, so borrowing doesn’t seem as attractive. Since individuals also need to repay debts, spending is expected to decrease.

In an ideal world, higher interest rates bring prices back down due to less demand. But in practice, it can also cause deflation, which might be problematic in certain contexts.

Deflation

As you might guess, deflation is the opposite of inflation. We’ll define it as a general decline in prices over a period of time, typically caused by a decrease in spending. Since there’s less spending, it could further be accompanied by a recession (see The 2008 Financial Crisis Explained).

One proposed solution for deflation is the lowering of interest rates. By reducing the interest owed on credit, individuals are incentivized to borrow more. Then, with more credit available, the government anticipates that parties within their economy will increase their spending.

Like inflation, deflation can be measured through a Consumer Price Index.

➠ Looking to get started with cryptocurrency? Buy Bitcoin on Binance!

What happens when the economic bubble bursts?

Dalio explains that the chart we illustrated above (the short-term debt cycle) is a small cycle within the long-term debt cycle.

The long-term debt cycle.

The pattern described above (increasing and decreasing availability of credit) repeats itself over time. However, at the end of each cycle, there’s more debt. Eventually, the debt becomes unmanageable, triggering large-scale deleveraging (where individuals attempt to reduce their debt).This is represented by the sudden decrease on the chart.

When deleveraging occurs, incomes begin to drop, and credit dries up. Unable to repay debt, individuals attempt to sell their assets. But with so many doing the same thing, asset prices tumble due to an abundance of supply.

Stock markets crash in scenarios like this, and at this stage, the central bank can’t lower interest rates to alleviate the burden if they’re already at 0%. Doing so creates negative interest rates, which is a controversial solution that doesn’t always work.

So what can they do? Well, the most obvious way forward would be to decrease spending and forgive the debt. These bring other issues, though: reduced spending means that businesses won’t be as profitable, meaning that employees’ incomes will decrease. Industries will need to cut down on their workforce, leading to higher unemployment rates.

Then, lower incomes and smaller workforces mean that the government can’t collect as much tax. At the same time, it needs to spend more to provide for the increased number of unemployed citizens. Since it’s spending more than it’s receiving, it has a budget deficit.

A proposed solution here is to start printing money (making the money printer go brrrrr, as it’s known in cryptocurrency circles). With that money at its disposal, the central bank can lend to the government, which then attempts to stimulate the economy. But this can also lead to problems.

Creating money out of thin air causes inflation because it increases the money supply. This is a slippery slope that could eventually lead to hyperinflation, where inflation accelerates so fast that it destroys the value of a currency and results in economic disaster. You need only look to the examples of the Weimar Republic in the 1920s, Zimbabwe in the late 2000s, or Venezuela in the late 2010s to see the impact hyperinflation can have.

When compared to the short-term cycles, the long-term debt cycle plays out across a much longer time frame, believed to occur every 50 to 75 years.

How does it all tie together?

We’ve covered quite a few topics here. Ultimately, Dalio’s model revolves around the availability of credit – with more credit, the economy booms. With less credit, it contracts. These events alternate to create short-term debt cycles, which, in turn, make up part of long-term debt cycles.

Interest rates influence much of the behavior of the economy’s participants. When rates are high, saving makes more sense, as spending is not as much of a priority. When they’re lowered, spending appears to be the more rational decision.

Closing thoughts

The economic machine is so colossal that it can be difficult to wrap your head around its various components. However, by looking closely, we can see the same patterns repeating themselves over and over as participants engage in transactions with each other.

At this stage, you’ve hopefully got a better understanding of the relationship between lenders and borrowers, the importance of credit and debt, and the steps that central banks take to try and mitigate economic disaster.

That’s the much we can take on the topic “Ultimate Guide On How The Economy Works“.

Thanks For Reading

Common Cryptocurrency Scams on Mobile Devices

Ultimate Guide to Symmetric versus Asymmetric Encryption

How Blockchain Is Used in The Internet of Things (IoT)

Ultimate Guide to Understanding What Makes a Blockchain Secure

Upto Date Blockchain Use Cases

Initial Coin Offering List – Comprehensive List of Projects Currently Doing ICO

Ultimate Guide to Initial Coin Offering (ICO)

Ultimate Guide to Understanding What Fractional Reserve is

Understanding Why Public WiFi Is Insecure

The Ultimate History of Cryptography

Understanding what DoS Attack is

Ultimate Guide to what Fiat Currency is

Ultimate Guide to zk-SNARKs and zk-STARKs

Things to Avoid When Using Binance Chain

How Blockchain Is Used In Charity

How Blockchain is Used in Supply Chain

Ultimate Guide to What a Replay Attack is

Ultimate Guide to Delegated Proof of Stake

Ultimate Guide to what Ransomware is

Ultimate Guide to understanding Cryptojacking

Ultimate Guide to Understanding Inflation for Beginners

How to Know Cryptocurrencies Pyramid and Ponzi Schemes

Ultimate Beginner’s Guide to Bitcoin’s Lightning Network

Advantages and Disadvantages Of Blockchain

Ultimate Guide to Ethereum Plasma

Leave a Reply